May 15, 2026

- A SAS Aviation Insights analysis of RefuelEU Aviation shows e-SAF mandates from 2030 will expose a major supply gap, with Scandinavia alone requiring roughly 36,000 tonnes initially, rising to about 330,000 tonnes by 2040, equivalent to scaling from one production plant to around five dedicated facilities.

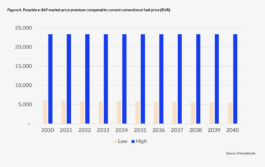

- The economics are highly sensitive to supply conditions: in a constrained market, e-SAF prices could approach non-compliance levels near €23,000 per tonne versus conventional jet fuel at roughly €700–€750 per tonne, while even a well-supplied market still implies a premium of around €6,000 per tonne in 2030.

- Total regional costs are projected to escalate sharply, from €225–€850 million in 2030 to as much as €7.8 billion by 2040, translating into passenger-level surcharges of roughly 27–130 DKK in Denmark, 28–107 NOK in Norway and 34–130 SEK in Sweden in 2030 alone, with regulatory penalties and limited production capacity raising the risk of sustained shortages across Europe.

A new SAS Aviation Insights report puts hard numbers on what Europe’s sustainable fuel mandate will actually cost, and the gap between what’s required and what exists today is wider than most in the industry have publicly acknowledged.

The introduction of the e-SAF blending mandate under RefuelEU Aviation in 2030 is no longer a distant policy ambition.

A detailed analysis published by SAS in April 2026, authored by Thomas Thessen, Chief Analyst at SAS, attempts to quantify what that gap looks like specifically for Scandinavia: the volumes of e-SAF that will be required year by year, the range of prices the market might clear at, and what those costs ultimately translate to for airlines and for passengers.

What e-SAF is and why it’s different

Understanding the cost challenge starts with understanding the fuel itself. e-SAF, electrofuel or Power-to-Liquid (PtL) SAF, is produced from renewable electricity, water and captured CO₂.

Electricity and water are converted into hydrogen via electrolysis; that hydrogen is then combined with CO₂ to produce syngas, which is refined into aviation fuel through either the Fischer-Tropsch synthesis route or the Methanol-to-Jet pathway, the latter currently advancing through ASTM D4054 certification. Unlike bio-based SAF pathways such as HEFA, currently the most widely produced SAF type, derived primarily from used cooking oil and waste fats, PtL fuels do not depend on biomass feedstocks.

That makes them one of the most scalable long-term options for expanding sustainable aviation fuel supply. Under RefuelEU Aviation, e-SAF is classified as a Renewable Fuel of Non-Biological Origin (RFNBO).

“The EU has allocated 20 million aviation ETS allowances to support SAF purchases from 1 January 2024 to 31 December 2030. The most commonly used SAF pathway today, HEFA, can receive support covering 50 percent of the price difference between conventional jet fuel and SAF, based on annual average price levels estimated by EASA (European Union Aviation Safety Agency). Once e-SAF enters the market, it will be eligible for support covering 95 percent of the price differential. The 20 million allowances are expected to be exhausted by 2027–2028, after which the EU may decide whether to extend the support scheme. For the purposes of this report, it is assumed that the support scheme will not be continued beyond its current allocation,” written in a report.

The distinction matters commercially because e-SAF carries its own dedicated sub-mandate within RefuelEU — separate from, and additional to, the broader SAF blending requirement, with its own penalty structure for non-compliance.

Main insights

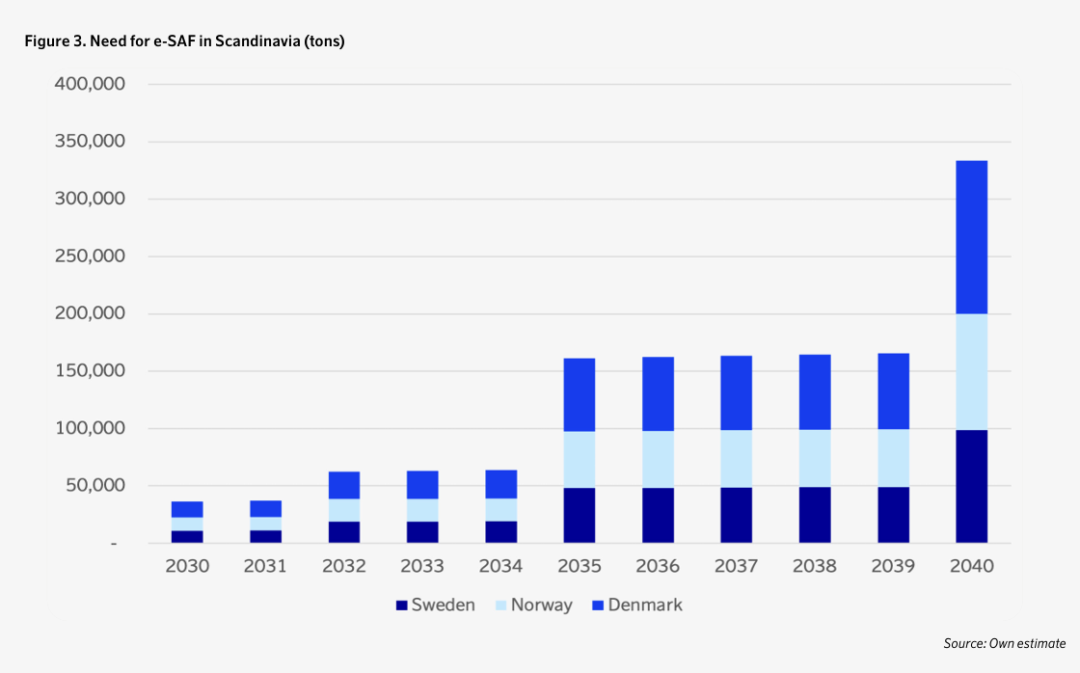

The e-SAF blending mandate begins in 2030, creating a requirement for approximately 36,000 tonnes of e-SAF across the three Scandinavian countries. By 2032, this demand increases to more than 60,000 tonnes and when the mandate rises to 5% in 2035, the need reaches around 160,000 tons, growing further to approximately 330,000 tonnes by 2040.

This would require the output of one dedicated plant by 2032, increasing to 2–3 plants by 2035 and around 5 plants by 2040. • The market price of e-SAF will mostly depend on whether the market is short (supply below demand) or long (demand below supply)

“In a short market the e-SAF price will in theory be close to the cost of non-compliance. This could result in a premium price of around €23,000/tons. This can be compared to the normal price of conventional fuel of €700–€750/tons • Based on a cost price estimated by EASA in 2025, the market price premium in a long market would in a best-case scenario be around €6,000/tons in 2030,” mentioned in a report.

The total cost of e-SAF in Scandinavia in 2030 will based on the assumptions above be between €225 million and €850 million. This will in 2035 increase to €950–€3,800 million, and €1,850 million–€7,800 million in 2040. • The cost per passenger in Denmark will be 27–105 DKK in 2030, 104–421 DKK in 2035 and 189–803 DKK in 2040. • The cost per passenger in Norway will be 28–107 NOK in 2030, 105–424 NOK in 2035 and 190–806 NOK in 2040. The cost per passenger in Sweden will be 34–130 SEK in 2030, 129–520 SEK in 2035 and 233–989 SEK in 2040.

Scandinavia’s e-SAF volumes

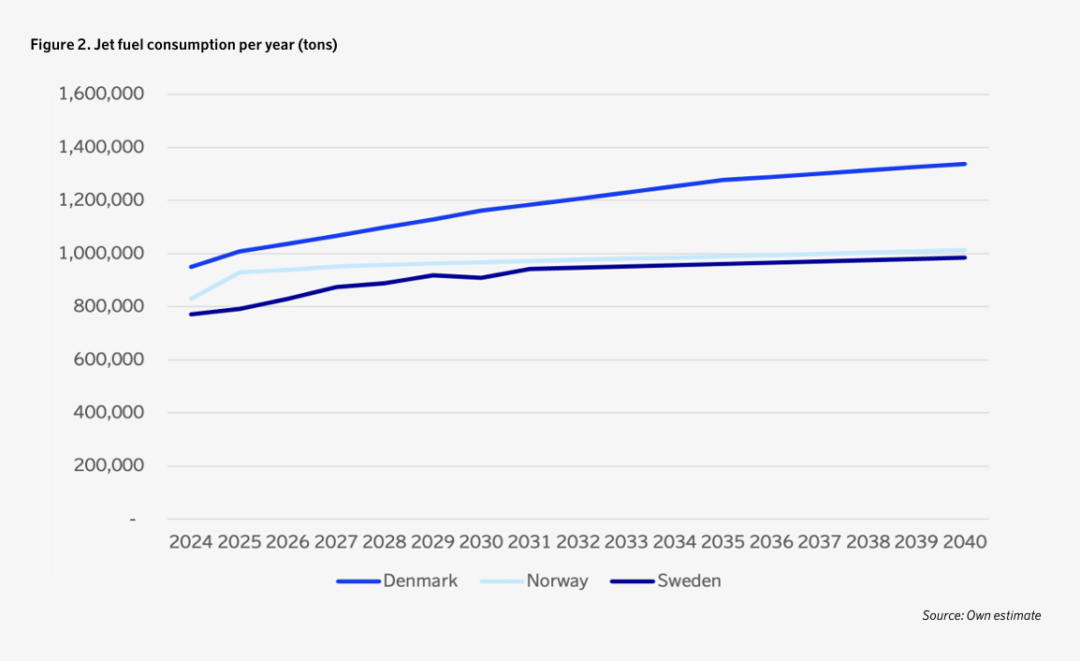

The SAS analysis defines Scandinavian e-SAF need as the volume of jet fuel uplifted within the three countries, Denmark, Norway and Sweden. Total jet fuel demand across the region is projected to reach 3.0 million tons in 2030 and 3.3 million tonnes by 2040. Applying the EU blending mandate percentages to those volumes produces the following e-SAF requirements:

- 2030: approximately 36,000 tonnes (1.2 percent mandate)

- 2032: more than 60,000 tonnes (2 percent mandate)

- 2035: around 160,000 tonnes (5 percent mandate)

- 2040: approximately 330,000 tonnes

In infrastructure terms, current expectations point to future e-SAF production facilities having an average annual output capacity of 60,000 to 70,000 tonnes. On that basis, Scandinavia alone would need the equivalent of one dedicated plant fully operational by 2032, two to three plants by 2035, and around five plants by 2040.

The report notes that meeting the EU-wide requirement in 2030 will demand approximately 552,000 tonnes across the EU and EEA, implying around eight new production facilities at scale needing to be operational by that point. By 2035, that rises to more than 35 facilities.

The passenger forecasts underpinning these volume calculations vary by country. Denmark is projected to grow from 19 million departing passengers in 2025 to 29 million in 2040, based on historical trends and SAS’s own growth strategy at Copenhagen Airport. Norway’s jet fuel demand is modelled using GDP forecasts from SSB combined with a historical passenger-to-GDP elasticity of 1.1. Sweden’s figures are based on the Transportstyrelsen forecast through 2031, with an assumed annual growth rate of 1.7 percent thereafter.

“As no Final Investment Decisions (FIDs) have yet been taken for any European e-SAF projects, there is a substantial risk that the market will be ‘short’ when the blending mandate comes into effect in 2030. Meeting the EU-wide requirement will demand approximately 552,000 tonnes of e-SAF in all of EU/EEA in 2030, implying that around eight new e-SAF production facilities would need to be operational by that time to avoid a supply shortage,” written in a report.

By 2035, this requirement would rise to more than 35 facilities. Under the current regulation, penalties for non-compliance must be at least twice the price difference between conventional fuel and e-SAF. Germany has already proposed a penalty level of €17,000 per ton, even though EASA’s price estimates indicate that the minimum penalty required under the regulation would be €13,922 per ton. Suppliers must still compensate for the shortfall by meeting the missed obligation in the following year. It is stated in the regulation that double penalty must be avoided.

“In a short market lasting for more than one year, this must result in the total cost of non-compliance to be the penalty for the first year equal double the price premium, plus one time the price difference in year two11. In total three times the price premium. In a short market, fuel suppliers are expected to be willing to pay a price just below the penalty level, as doing so reduces their overall compliance costs. In practice, a willingness to pay around 10–15 percent below the penalty is anticipated, reflecting the additional handling and operational costs associated with receiving and using e-SAF.”

The post Scandinavia’s e-SAF reckoning appeared first on Air Cargo Week.

Go to Source

Author: Anastasiya Simsek

Latest Posts