May 06, 2026

- Fuel prices are climbing sharply across key global markets, adding fresh cost pressure to already strained logistics and air cargo supply chains.

- With Brent crude trading near USD 126, its highest level since late February, diesel prices have surged in parallel, rising by more than 40% in the US and breaching EUR 2 per litre across much of Europe.

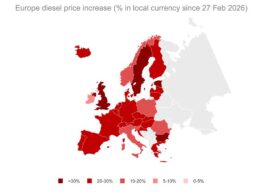

In the United States, the national average diesel price reached USD 1.45 per litre by 29 April, up around 42% since 27 February. Across Europe, prices have also climbed, with the average hitting EUR 2.02 per litre. The Netherlands leads the region at EUR 2.4, followed by Denmark, Finland, Germany and France, according to IRU.

Elsewhere, diesel prices are around 21 percent above pre-war levels in China, while Brazil and Mexico have recorded increases of 19% and 7% respectively. Türkiye remains an outlier, with prices easing slightly week-on-week despite a broader upward trend since February.

Pump prices

The US national average diesel price reached USD 1.45 per litre on 29 April, up around 42% since 27 February. The US has so far not suspended or reduced the federal diesel excise tax.

The Brent–WTI spread has widened to around USD 15 per barrel, with domestic crude pulling into US refinery runs to partly offset Middle East shortfalls.

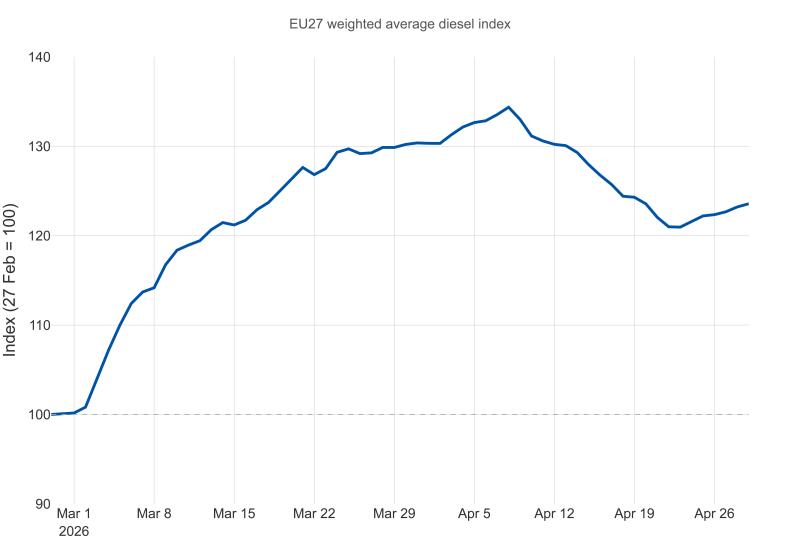

In the EU, the average diesel price hit EUR 2.02 on 29 April, up from EUR 1.98 on 24 April.

The Netherlands retains the highest pump price at EUR 2.4 per litre, followed by Denmark, Finland, Germany and France, while Malta remains unchanged at EUR 1.210 per litre thanks to its regulated price structure. Excluding Malta, Spain and Poland have the cheapest average pump prices.

Upcoming national fiscal actions:

- Austria – Austrian mineral tax is renewed monthly. The current EUR 0.5 per litre cut on petrol (EUR 0.43 per litre applied tariff) and diesel (EUR 0.34 per litre applied tariff) is set to expire on 30 April absent a renewal communiqué that has not yet been published.

- France – the TotalEnergies voluntary cap (EUR 2.25 per litre diesel, EUR 1.99 per litre petrol) at 3,300 stations is anchored to 30 April. No fresh extension communiqué has been issued. The separate fuel discount privileged cap (EUR 1.99 per litre, all fuels for E&G clients) runs the full year independently. The EUR 50 million government envelope for road transport for April and the tanker-circulation derogation extended to 11 May remain in force.

- Germany – petrol and diesel excise will be cut by EUR 0.14 per litre for the period 1 May to 30 June, paired with the previously announced one-price-increase-per-day retail rule in force since 1 April. The law is awaiting promulgation by the Federal President and publication in the Bundesgesetzblatt (Federal Law Gazette); pump pass-through from Friday is the next data point to track.

- Greece – the EUR 0.20 per litre diesel pump subsidy was formally extended through May on Monday 27 April.

- Hungary – the cap on petrol and diesel prices (HUF 595 per litre petrol / HUF 615 per litre diesel) expires on 1 May. No formal review beyond that date is visible in the Magyar Közlöny as of this morning. The Druzhba flow restart on 23 April has eased Hungarian wholesale diesel quotations, narrowing the gap to the retail cap for the first time since 9 March.

- Italy – the Council of Ministers is expected to decide on Thursday 30 April on whether to renew DL 42/2026 (the EUR 0.20 per litre excise cut) beyond 1 May. Without action, the automatic excise reset takes effect on Saturday 2 May.

- Poland – Minister of Finance regulations published on Monday 27 April extended the reduced VAT (8% versus statutory 23%) and the EU-minimum excise (–29 gr/L petrol, –28 gr/L diesel) on motor fuels from the original 30 April expiry to 15 May 2026. The daily PLN 7.60 per litre diesel cap remains unchanged, and the Sejm (lower house of the Polish parliament) option to push the regime to 30 June 2026 remains available. The Polish package therefore now overlaps the German Tankrabatt and the Swedish energy tax cuts that take effect on 1 May.

- Sweden – the spring budget fuel-tax package takes effect on 1 May. Diesel energy tax is reduced by SEK 319 per cubic metre and petrol energy tax by SEK 0.82 per litre, in force through 30 September.

In Türkiye, diesel prices are down by around 2% week on week and up around 18% in Turkish lira since 27 February.

In China, diesel is around 21% above the pre-war baseline. Beijing continues to prioritise domestic supply over state-owned refiner margins; export restrictions on refined products remain in place. China is particularly exposed to the Hormuz route, with around 57% of crude imports coming from the Middle East.

In Brazil, retail diesel is at BRL 7.21 per litre, up 19% on the BRL 6.08 baseline of 27 February. The PIS/Cofins zero rating on diesel and the BRL 0.32 per litre subsidy remain in force, and a 50% diesel export tax is in place. Localised shortages continue in the Centre-West.

In Mexico, diesel retail is on average at MXN 28.08 per litre, a 7% increase since 27 February. The Ministry of Finance has reduced its diesel stimulus from 43.17% to 33.22%. The next IEPS publication (a federal excise tax applied to specific goods) for the week of 2–8 May is expected on Friday 1 May. Bloomberg Línea’s 21 April assessment that the fuel subsidy cost has grown about twice as fast as the extra oil-export revenue since the start of the crisis is the first material signal that the Mexican fiscal cushion is wearing thin.

AdBlue prices remain the secondary pressure point. Global urea prices remain above USD 684 per tonne (30 April), around 47% above the 27 February baseline. AdBlue retail prices have jumped by around 20% in Belgium, with similar moves reported by Italian operators. While AdBlue accounts for less than 1% of overall TCO, shortages would be catastrophic for operators given its mandatory use on modern diesel fleets.

The post War-driven fuel surge sends global freight costs higher appeared first on Air Cargo Week.

Go to Source

Author: Anastasiya Simsek

Latest Posts