Apr 07, 2026

- Global freight markets are being reshaped by a combination of geopolitical disruption and rising fuel constraints, with both ocean and air cargo sectors feeling the impact, according to analysis shared by Freightos.

- Nearly six weeks after Iran closed the Strait of Hormuz, vessel traffic through the key maritime chokepoint remains severely restricted, with only a handful of ships transiting daily. Notably, a CMA CGM vessel became one of the first major European carrier ships to pass through under coordinated conditions, highlighting the complexity of current operations.

Air cargo markets are once again being pulled by forces outside their control. Nearly six weeks into the disruption around the Strait of Hormuz, the impact is no longer confined to ocean freight. Instead, tightening fuel availability, constrained capacity and shifting trade flows are feeding directly into air cargo pricing and network dynamics, creating a more complex operating environment for carriers and forwarders alike. While container shipping has borne the immediate brunt of restricted vessel movements, the knock-on effects are increasingly visible in air freight.

Fuel has moved to the centre of the discussion

Reports of limited jet fuel availability in parts of Asia, including flight cancellations in Vietnam and refuelling restrictions in South Korea and the Philippines, underline how quickly operational constraints can emerge.

At the same time, Middle Eastern carriers, which play a pivotal role in connecting East–West flows, are still in recovery mode. Capacity remains below normal levels, with Emirates SkyCargo estimated at around 60 percent of its typical schedule, Etihad at 40 percent and Qatar Airways Cargo at approximately 20 percent. This shortfall continues to shape global air cargo flows, particularly across Asia–Europe and Europe–Middle East lanes.

The immediate response to disruption has been a sharp rise in rates. Freightos Air Index data show South Asia–Europe prices up 62 percent compared to pre-conflict levels, while Southeast Asia–Europe rates have climbed 33 percent to around $4.50 per kg. Europe–Middle East rates have effectively doubled.

In recent weeks, signs of stabilisation have emerged. Rates on key lanes have begun to level off, with China–Europe prices down 7 percent over the past fortnight and Southeast Asia–Europe rates easing by around 10 percent from recent highs. This suggests that initial shock-driven demand has started to normalise as capacity is gradually reintroduced and supply chains adjust.

For forwarders, this creates a more nuanced environment. Pricing remains elevated, but less volatile than in the immediate aftermath of disruption. The question is no longer whether rates will spike, but how long they can be sustained.

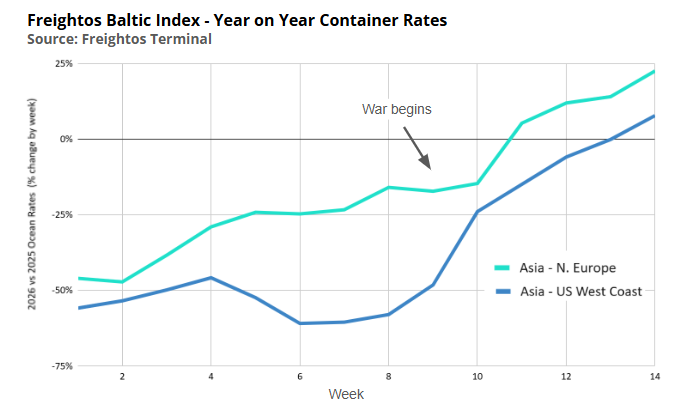

The interaction between ocean and air markets remains critical. Container rates have surged despite weak underlying demand, with transpacific prices up nearly 40 percent since before the conflict and Asia–Europe rates rising by around 20 percent. Under normal conditions, this period between Lunar New Year and peak season would see rates soften. Instead, higher fuel costs and constrained vessel movements have reversed that trend. With only a limited number of ships transiting the Strait of Hormuz—and in some cases requiring coordination or pre-arranged payments—ocean supply chains are under pressure.

The post How fuel shortages and war-driven disruption reshape air cargo flows appeared first on Air Cargo Week.

Go to Source

Author: Anastasiya Simsek

Latest Posts