Oct 03, 2023

While general cargo tonnages have fallen in all of the main world origin regions, WorldACD highlights a number of areas recording tonnage increases during the first 8 months of 2023, including certain important product categories, origin points, and world regions or sub-regions

Special air cargo product verticals have continued to record growth in the first eight months of 2023, while general cargo tonnages have fallen, year on year (YoY), from all of the main world origin regions, new analysis from WorldACD Market Data has revealed. Total worldwide chargeable weight flown from January to August 2023 was down -7% compared with the equivalent period last year, although the YoY gap has continued to narrow as the year has progressed, dropping to -3% for July and August combined. But analysis by WorldACD of the more than 2 million monthly transactions captured in its database highlights a number of areas that have continued to achieve growth at various times this year, including certain important product categories, origin points, and world regions or subregions.

Product category performancesExamining the performance of some of the major air cargo product categories so far this year, WorldACD identified big declines in express (-17%), general cargo (-12%), and dangerous goods (-12%) in the January-August period, compared with last year, while pharma/ temperature-controlled shipments remained characteristically stable during this period. But there was notable growth for vulnerable/high tech (+7%), live animals (+5%), perishables (+4%), and valuables (+2%) shipments, compared with January-August 2022.

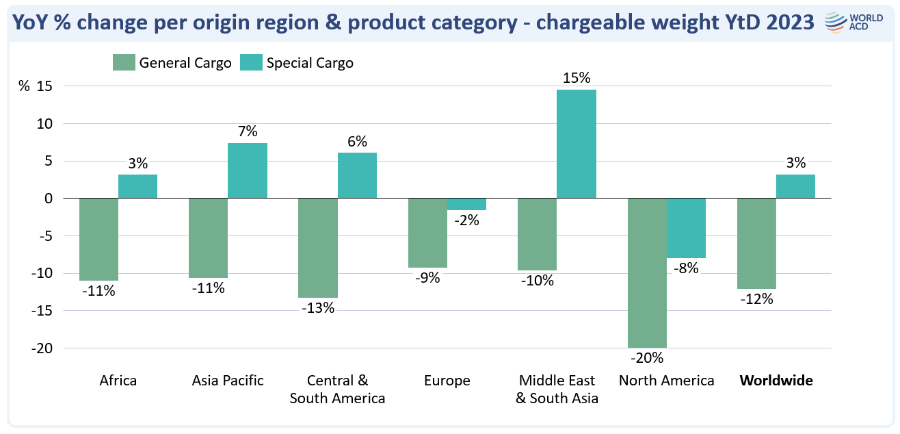

Combined figures for all the special cargo product verticals categories recorded by WorldACD indicate that tonnages of special cargo products as a whole grew by +3% on a worldwide year-to-date (YtD) basis, whereas general cargo tonnages fell by -12%, YoY, in those first 8 months of 2023.Examining this separation of general cargo and special cargo on a regional basis is also revealing, with general cargo tonnages significantly down, YoY, from all of the main origin regions, in most cases recording double-digit declines of between -10% and -20%, with Europe the only slight exception (-9%). In contrast, special cargo product verticals recorded growth from all of the main regions except North America (-8%) and Europe (-2%), ranging from +3% from Africa, +6% from Central & South America, +7% from Asia Pacific, to +15% from Middle East & South Asia.

Combined figures for all the special cargo product verticals categories recorded by WorldACD indicate that tonnages of special cargo products as a whole grew by +3% on a worldwide year-to-date (YtD) basis, whereas general cargo tonnages fell by -12%, YoY, in those first 8 months of 2023.Examining this separation of general cargo and special cargo on a regional basis is also revealing, with general cargo tonnages significantly down, YoY, from all of the main origin regions, in most cases recording double-digit declines of between -10% and -20%, with Europe the only slight exception (-9%). In contrast, special cargo product verticals recorded growth from all of the main regions except North America (-8%) and Europe (-2%), ranging from +3% from Africa, +6% from Central & South America, +7% from Asia Pacific, to +15% from Middle East & South Asia.

READ: Menzies Aviation sign agreement with Air Serbia to support airline’s growth

Product pricing variation There has also been considerable pricing variation this year between general cargo and special cargo products categories, especially regionally, although each are down significantly on a worldwide and regional basis. Nevertheless, special cargo rates (-30%) have held up better than general cargo rates (-38%) on a worldwide basis, compared with the first 8 months of last year. It is worth noting that rates for perishables have not come down as much, but they also did not increase as much as other product categories during the Covid years. That pricing differential is particularly apparent ex-Africa, where general cargo rates are down -23%, YoY, in the first 8 months, whereas special cargo pricing has dropped just -7%. Pricing ex-Central & South America, another market where perishables form a big component, is down -18% for general cargo, compared with just -8% for special cargo. In contrast, the substantial YoY fall in prices ex-Asia Pacific has been shared almost equally among general cargo (-44%) and special cargo (-41%) shipments in the first 8 months of this year.

Regional tonnages stabiliseBut overall tonnages flown from Asia-Pacific have been holding up much better, YoY, in recent months than at the start of 2023, as they have on most worldwide markets, as demand has stabilised. After declining, YoY, in the first two quarters of 2023, tonnages flown from Asia Pacific returned to positive territory in July and August combined, recording +3% growth. Chargeable weight flown from Middle East & South Asia also recorded growth (+4%) in July and August, having dropped -7% in the first quarter (Q1) and fallen slightly (-1%) in Q2.

Volumes from Africa, and from the Central & South America have been more or less flat, compared with last year, in the first 8 months, but tonnages from North America (-17%) and from Europe (-7%) remained down significantly – including in the July-August period (-15% and -8%, respectively).Mexico leads subregion growthIn its second-quarter (Q2) and first-half (H1) analysis, WorldACD analysed outbound tonnages from various world subregions, highlighting North Africa as the fastest-growing origin subregion in the first half of 2023, recording +21% growth. But in this latest YtD analysis, covering January to August, WorldACD examined those same subregions on a combined outbound and inbound basis, identifying Mexico as the fastest-growing overall area during this period, with +10% growth, YoY.

Other growth areas included Caribbean (+7%), Central Africa (+6%), North Africa (+5%), China (+3%), the Gulf area (+2%), and the Levant & Caucasus (+1%). West Africa, Central America, and Balkans and Southeast Europe were more or less flat as subregions during the first eight months of the year.But on the other end of the scale, big declines can be seen in other parts of Asia, with Northeast Asia (excluding China, -16%) and Southeast Asia ( -15%) the worst-performing subregions during this period. Other subregions recording significant declines include USA (-11%), East Africa (-10%), Australasia & Pacific (-10%), Western Europe (-7%), and Eastern Europe (-5%). Moderate declines were also recorded to and from Southern Africa (-4%), South America (-3%), Canada (-2%), Northern Europe (-1%), and South Asia (-1%).

READ: Wiremind is bringing next-level AI to its cargo products in 2024

Product origin championsFinally, WorldACD also identified the top three YtD growth origin countries or areas within several key product categories, with Hong Kong, South Korea, and China (South East) leading the growth in vulnerable/high-tech cargo shipments. India, Egypt and Brazil led the growth in fruits and vegetables shipments, with Ecuador, Columbia, and Kenya topping the list of countries achieving growth in chargeable weight of flower shipments. Chile, the UK, and Argentina led the way in fish and seafood export tonnage growth, while India, the Netherlands, and Italy topped the growth origin countries for temperature-controlled/pharma products.

Meanwhile, China (East), UAE, and Canada (East) led the growth in dangerous goods exports, with Brazil, the Philippines, and Indonesia, leading growth in outbound live animal air shipments. And finally, Hong Kong, Greece, and Japan were the biggest growth sources for valuables shipments in the first 8 months of this year, compared with the equivalent period in 2022, in terms of absolute increases in chargeable weight.

The post Special air cargo verticals see continued growth in 2023 appeared first on AIR CARGO WEEK.

Go to Source

Author: Edward Hardy

Latest Posts