Aug 09, 2023

Analysis by WorldACD highlights areas recording ongoing growth and interesting demand and pricing patterns in the second quarter and first half of 2023

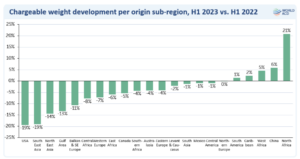

North Africa is among just a handful of global air cargo origin subregions to record growth in the first half of 2023, according to analysis by WorldACD Market Data, amid a wider overall picture of declining year-on-year (YoY) chargeable weight and average rates on most markets.The public available report by the air cargo data specialist, based on the 2 million monthly transactions covered by WorldACD’s data, compares the second quarter (Q2) and the first half (H1) of 2023 with the equivalent periods last year and in 2019, the last pre-Covid year, highlighting a number of areas recording ongoing growth and interesting demand and pricing patterns, as markets continue their post-Covid readjustments. It reveals, for example, that chargeable weight from North Africa in the first 6 months of this year rose by +21%, YoY, with China (+6%), West Africa (+5%), Caribbean (+2%) and South America (+1%) the only other origin subregions to register positive growth compared with the equivalent H1 period last year.

Subregions remaining relatively stable include Northern Europe (0%), Central America, Mexico, and South Asia (-1%), with single-digit percentage declines also recorded for Eastern Europe (-4%), Australia & Pacific (-4%), Southern Africa (-4%), Canada (-5%), East Africa (-6%), Central Asia (-7%), Western Europe (-7%), and Central Africa (-8%). Origin subregions recording particularly steep declines include USA and Southeast Asia (-19%), Northeast Asia (-14%), the Gulf area (-13%), and Balkan & Southeast Europe (-11%). Global tonnages down -9% in H1On a global basis, chargeable weight in H1 was down by almost -9%, YoY, driven regionally by a sizeable (-18%) drop in tonnages from North America and from the big Asia-Pacific origin region (-9%), with significant drops ex-Europe (-7%) and from the Middle East & South Asia region (-4%). On a full regional basis, only Central & South America (+1%) recorded any YoY growth in the first half of 2023, with tonnages ex-Africa stable.

Growth continues in vulnerables, valuables, perishables, and live animalsMeanwhile, a handful of product categories have continued to record YoY growth this year on a global basis in the first 6 months, notably Vulnerables/High-tech (+3%), Valuables (+3%), Perishables (+4%), and Live Animals (+11%). Pharma/Temperature-controlled products stayed more or less stable (-1%), but there were double-digit percentage drops in volumes of Dangerous Goods (-10%), General Cargo (-14%), and Express (-20%).

Developments in Q2While worldwide tonnages were down by almost -9% in H1, the comparison moderated to -6% in Q2, YoY, although tonnages have now fallen -9% below their pre-Covid levels of Q2 2019. Capacity, meanwhile, has now recovered to its pre-Covid levels in Q2 2019, having risen by +11% compared with Q2 last year.On the pricing side, average air cargo rates in the second quarter of 2023 were down by -40%, YoY, although they remain significantly above pre-Covid levels (+34% compared with Q2 2019).

Those rate and demand patterns are also illustrated well if we examine the world’s top 10 air cargo trade lanes (based on chargeable weight). Demand in the second quarter of 2023 was below its levels in the equivalent period last year, and below 2019 pre-Covid levels on most major lanes, with the exception of Asia Pacific to North America (up vs 2022 and 2019) and Central & South America (CSA) to North America (up vs Q2 2019), and Asia Pacific to Middle East & South Asia (MESA), up vs 2022. However, average yields on all of the world’s top 10 international air cargo markets were significantly higher in Q2 this year than their 2019 pre-Covid levels, although they were down vs last year’s levels.

Fuel surcharge componentOne component of the elevated prices compared with pre-Covid levels has been higher fuel surcharges, partly resulting from the rise in jet fuel prices since Russia’s invasion of Ukraine. Although jet fuel prices as well as air cargo fuel surcharges remain significantly above their levels in January 2019 (+34% for the fuel surcharge in May 2023 on Asia Pacific to Europe routes, and +54% on Asia Pacific to North America), jet fuel prices and cargo surcharges have dropped back close to their levels in early 2022.

Spot vs contract rates balance in Q2One interesting development in the second quarter of 2023 has been a slight shift back in favour of contract rates. That follows a progressive trend over much of the last year in which customers bought an increasing share of their business via the spot market, after spot prices dropped below contract prices on many lanes by mid-2022.

Although average spot prices remain somewhat below average contract rates (around 15% lower in June 2023, globally), the shift towards the spot market appears to have halted since Q2, with a roughly 50-50 split now between spot and contract pricing, globally – although that split varies significantly between trade lanes. On Asia-Pacific to Europe, the share of spot prices increased in the final quarter of 2022 well above 50%, peaking at more than 55% last November and remaining above 50% throughout Q1 2023. However, by Q2 of this year, that proportion had dropped significantly to around 45% of the market, as customers increasingly sought the stability of contract pricing.On transpacific markets, the picture is less clear in a more-volatile market that has seen big price disparities at certain times in the last 12 months between the levels of contract rates and spot rates. The chart below illustrates how customers have made greater use of the spot market during periods of particularly wide spreads between spot and contract pricing – for example, between October 2022 and January 2023, when the share of spot rates peaked at more than 74%. But that share has dropped somewhat this year as the price gap has narrowed, stabilising in Q2 at around two thirds of the market.

The post North Africa tops air cargo growth appeared first on AIR CARGO WEEK.

Go to Source

Author: Edward Hardy

Latest Posts