Mar 08, 2024

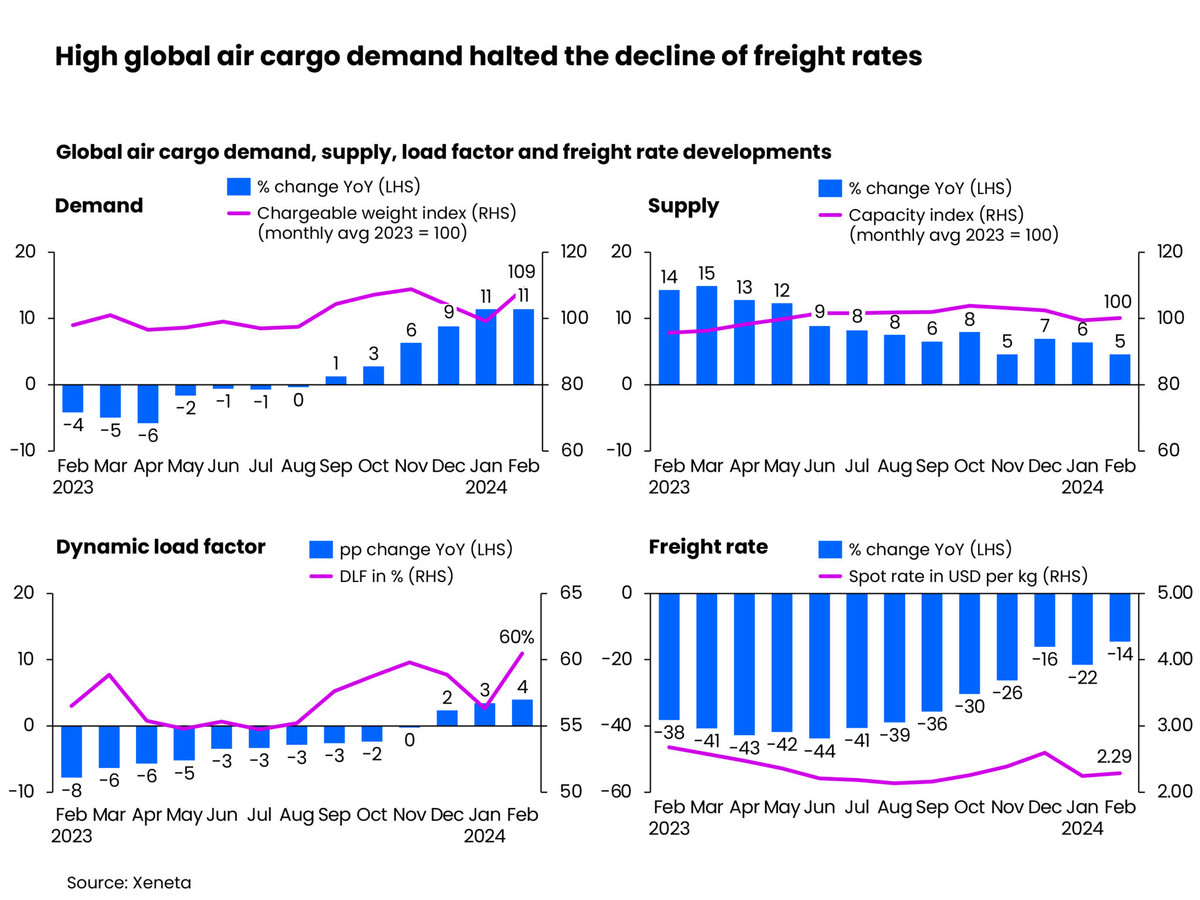

The global air cargo market’s surprisingly positive start to 2024 continued in February with a second consecutive month of double-digit growth in demand and an uptick in general freight spot rates, according to Xeneta’s latest weekly market analysis.

READ: International Women’s Day 2024: The crucial role of inclusion in logistics

Following January’s 11% volume growth, February saw a similarly welcome upward curve for airlines and freight forwarders, with demand increasing +11% year-over-year. Reflecting this improvement, in what is traditionally a slower time of year for airfreight volumes, the average global cargo spot rate in February rose +2% from the previous month to USD 2.29 per kg.

This increase is unusual compared to pre-pandemic trends during the same periods. Traditionally, air cargo spot rates tend to decline following the year-end peak season in the previous year and immediately after the Lunar New Year before rebounding towards the year-end holiday season this year.

“It’s a surprising start to the year from a volume perspective and not something people would have expected, ourselves included, with demand much higher than a year ago. Generally, we wouldn’t expect a rate uptick at this time of year. This is likely related to the Red Sea disruption, but this is not the only factor,” said Niall van de Wouw, Chief Airfreight Officer at Xeneta. “Signals suggest inflation is not cooling because consumers are still spending. It’s not how much they spend boosting airfreight; it’s where they finish. Trends indicate more consumers are buying on e-commerce platforms, and the intercontinental nature of these businesses and the speed with which they are expected to deliver benefit air cargo. For some airlines, e-commerce makes up over 50% of their revenue ex-East Asia.

“We now wait to see what impact the airline’s summer schedules will have and what happens next in the Red Sea. We would expect to see downward pressure again on rates once the summer belly capacity returns in the western hemisphere and China, where the travel recovery is by no means yet done,” he said.

The growth in global air cargo traffic in February, measured in chargeable weight, rose +10% month-over-month, pushing the global dynamic load factor up by four percentage points to 60%. International air cargo capacity remained relatively unchanged from the previous month. Xeneta’s emotional load factor analyses the volume and weight perspectives of cargo flown and the available capacity.

The increase in the average general cargo spot rate in February and the upward trend in volume for the first two months of 2024 were most likely driven by the substantial growth in demand caused by the Red Sea disruption and e-commerce demand from China. Some operators even imposed short-term embargoes on import traffic ex Asia during February to help clear backlogs caused by the sudden surge in air cargo volumes as demand growth outpaced the growth of global cargo supply (+5% year-on-year) for the fourth consecutive month.

Consequently, the year-on-year decline of the global air cargo spot rate reached its lowest level since October 2022 in February, at -14 %.

The ongoing conflict in the Red Sea continues to impact ocean container shipping, producing a positive spillover modal shift in favour of air cargo. According to Sea Intelligence, recent declines in ocean container spot rates were also affected by a drop in ocean schedule reliability for Asia-to-Europe trades, recorded at 39.4% in January, the lowest level since October 2022. This has further contributed to the substantial increase in air cargo demand on this corridor for shippers willing and able to bear the higher airfreight cost to maintain the resilience of their supply chains.

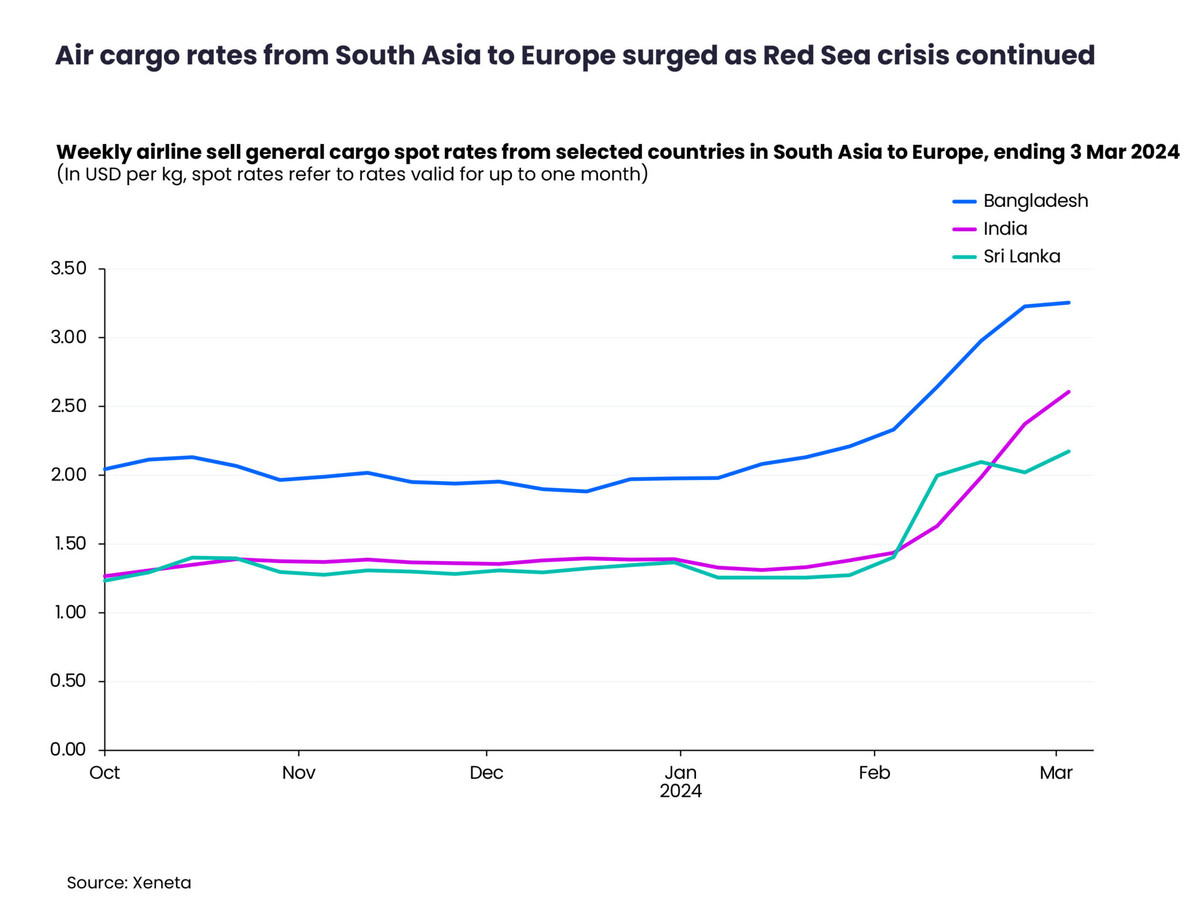

In February, the South Asia to Europe market led the month-over-month growth in spot rates. The situation in the Red Sea caused air cargo demand on this trade to rise by +18% from the previous month, lagging one month behind the demand growth for China and Vietnam to European markets. Consequently, the average spot rate from South Asia to Europe increased by +34% month-over-month to USD 2.15 per kg in February.

Looking at the general cargo market at a country level, India, Bangladesh, and Sri Lanka experienced significant increases in their prevailing cargo spot rates, which rose by a considerable +81%, +40%, and +55%, respectively, in the week ending on 3 March, compared to four weeks earlier, driven by strong demand for apparel products from these markets. Similar to the outbound South Asia market, the average spot rate from China to Europe rose by a more modest +11% month-over-month to USD 3.67 per kg in February – but the week-long Lunar New Year holidays caused a -9% decrease in the spot rate to USD 3.47 per kg in the week ending 3 March.

The air cargo spot rate from China to the US of USD 4.12 per kg in February was up +15% from January as spot rate changes stabilised throughout the month. In the week ending 3 March, the spot rate fell by only -2% from its peak in the week ending 11 February to just one cent below its monthly average of USD 4.12 per kg.

As the rise of cross-border e-commerce continues to drive demand for air cargo, particularly from Guangzhou and Hong Kong, market intelligence indicates some shippers transiting these locations are now considering and starting to use alternative hubs to circumvent capacity constraints caused by the e-commerce boom.

“Our conversations with shippers suggest many are looking to derisk their supply chains by avoiding hubs now dominated by e-commerce behemoths. This comes down to simple math for shippers. If you’re a clothing retailer, with spring on the way in Europe, you want your seasonal products in-store for the peak demand period. If they’re stuck in a sea container because of longer lead times, and you miss this opportunity, the subsequent markdown in the product cost is likely greater than switching from sea to airfreight. This is shaping the market – but we also know the market will probably surprise us again in the coming weeks,” van de Wouw said.

Compared to the previous corridors referenced, Europe to US air cargo spot rates saw the smallest month-over-month growth of +5% to USD 2.05 per kg in February.

Airlines, forwarders, and shippers will closely monitor market trends as airlines prepare to launch their summer schedules at the end of March. This will specifically impact the transatlantic air cargo market, which traditionally sees a capacity increase of about +50% due to increased belly capacity during the peak summer months for passenger travel. As in previous years, this change is expected to put downward pressure on air cargo rates on Europe-North America corridors and air cargo flows that use European hubs as transit points, such as those in the Indian subcontinent and Southeast Asia markets to North America.

Xeneta’s year-over-year analysis accounts for the 29-day month of February 2024.

The post Demand and rates for air cargo continued to rise in February appeared first on AIR CARGO WEEK.

Go to Source

Author: Anastasiya Simsek

Latest Posts