Mar 06, 2026

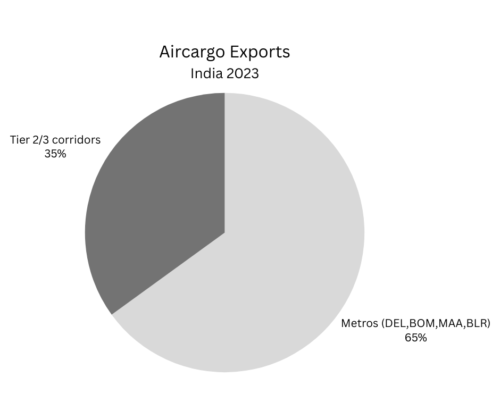

- India’s export growth is expanding beyond major metropolitan hubs, with around 35 percent of air cargo exports now originating from Tier 2 and Tier 3 manufacturing centres that depend on trucking and domestic connections to reach international airfreight capacity concentrated in Delhi, Mumbai, Bengaluru and Chennai.

- Structural constraints limit direct international cargo services from regional production hubs, including insufficient airport infrastructure, inconsistent customs procedures, cold-chain limitations and a freight forwarding market dominated by consolidators.

- Airlines are increasingly pursuing asset-light, partnership-driven strategies—using GSSAs, bonded trucking networks and domestic interline agreements—to aggregate inland cargo flows and access India’s growing export base without heavy infrastructure investment.

India’s export surge is increasingly being driven far beyond its largest cities, yet much of the global air cargo industry remains concentrated in the country’s major metropolitan gateways. As manufacturing expands across India’s industrial hinterland, a widening gap between export demand and available airfreight capacity is revealing a major opportunity for international carriers willing to rethink how they approach the market.

India recently crossed the US$4 trillion GDP milestone and continues to strengthen its position as a global export hub. From pharmaceuticals and textiles to engineering goods and perishables, Indian exporters are relying more heavily on fast and reliable airfreight connectivity to reach global markets.

However, while international demand for Indian exports continues to grow, direct uplift capacity from many production centres remains limited. Most long-haul cargo capacity is concentrated in four major airport gateways — Delhi, Mumbai, Bengaluru and Chennai — which together handle roughly 65 percent of the country’s air cargo exports.

The remaining 35 percent originates in Tier 2 and Tier 3 manufacturing centres across the country, where exporters rely on trucking and domestic connections to move goods to metro airports before they can be flown internationally.

For airlines seeking growth in one of the world’s fastest-expanding export markets, these underserved corridors represent a significant structural opportunity.

A market expanding beyond the metros

India’s air cargo market already exceeds 3.8 million tonnes annually, with an estimated value of more than US$12 billion. Driven by government initiatives such as “Make in India” and the Production Linked Incentive scheme, the sector is expected to expand significantly in the coming years, with volumes forecast to reach around 5.8 million tonnes by 2029.

A substantial share of that growth is emerging from industrial clusters located outside the country’s primary aviation hubs.

Pharmaceutical exports are concentrated in cities such as Hyderabad, Pune, Vadodara and Nagpur. Engineering goods production has expanded in hubs including Coimbatore, Rajkot and Sri City. Textile and garment manufacturing is heavily concentrated in cities such as Tirupur, Surat, Ludhiana and Moradabad.

Meanwhile, India’s perishables sector — including seafood exports from Trichy and agricultural products from Kerala and the northeast — depends heavily on reliable cold-chain logistics and rapid connections to international markets.

Despite the scale of production in these regions, direct international air cargo services remain limited, forcing exporters to rely on complex inland logistics networks to access global markets.

Structural barriers

Several operational factors continue to constrain the development of direct international air cargo services from secondary export hubs.

Infrastructure remains a major limitation. Many regional airports lack dedicated cargo terminals, freighter handling capabilities or adequate cold-chain facilities, making it difficult for airlines to establish direct international operations.

Regulatory and procedural inconsistencies also contribute to the problem. Exporters in certain cities face delays in customs clearance or duty drawback processing, which encourages routing shipments through larger airports where procedures are more predictable.

For time-sensitive shipments such as seafood, the reliance on long-distance trucking adds further complexity. Perishable cargo from Trichy, for example, can require more than six hours of transit before reaching an airport capable of handling international uplift.

The structure of the freight forwarding market also plays a role. In many cases, access to shipper volumes is mediated by large consolidators, creating limited transparency in pricing and complicating direct engagement between airlines and exporters.

Asset-light expansion strategies

Asset-light expansion strategiesRather than investing heavily in direct operations across numerous regional airports, airlines are increasingly exploring partnership-driven strategies to access India’s inland cargo flows.

General Sales and Service Agents (GSSAs) are central to this approach. These organisations typically combine regional sales networks with operational expertise in compliance, trucking coordination and shipper relationships.

In practice, successful models tend to incorporate several components. These include aggregating cargo demand from multiple inland production centres, building bonded trucking corridors that connect those locations with metro gateway airports, and forming domestic interline partnerships with Indian carriers to move cargo efficiently across the country.

By integrating these elements, airlines can expand their reach across India’s manufacturing base without the cost and complexity of establishing physical infrastructure in every production centre.

Evidence from emerging corridors

Examples from the market demonstrate how partnership-led models can unlock cargo flows from secondary manufacturing hubs.

Engineering exports from Sri City have been successfully consolidated and routed through Chennai or Bengaluru using coordinated trucking and sales networks. Such arrangements have enabled air lines to increase load factors while expanding the range of trade lanes served from these production centres.

Engineering exports from Sri City have been successfully consolidated and routed through Chennai or Bengaluru using coordinated trucking and sales networks. Such arrangements have enabled air lines to increase load factors while expanding the range of trade lanes served from these production centres.In the perishables sector, integrated trucking services have enabled seafood exports from Trichy to reach major international uplift points in Mumbai and Chennai within the required transit windows. This has allowed exporters to maintain consistent seasonal shipments while accessing global markets more efficiently.

These examples highlight how inland logistics integration can transform regional production centres into viable contributors to international air cargo networks.

The next phase of India’s air cargo growth

India’s Tier 2 and Tier 3 production centres already account for more than one-third of the country’s air cargo exports, and their share is expected to grow as manufacturing continues to expand beyond major metropolitan areas.

For global carriers, the opportunity lies not only in competing for capacity at India’s busiest airports, but also in developing deeper access to the industrial corridors that feed them.

Through closer collaboration with regional partners, expanded bonded trucking networks and flexible interline arrangements, airlines can tap into cargo flows that remain largely invisible in traditional network planning.

As India’s manufacturing footprint continues to diversify, these inland export corridors are likely to play an increasingly central role in shaping the country’s position in global air cargo markets.

The post India’s hidden air cargo corridors present major opportunity for global carriers appeared first on Air Cargo Week.

Go to Source

Author: Edward Hardy

Latest Posts